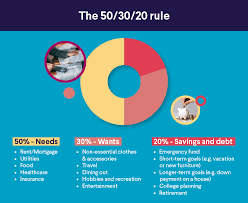

When it comes to managing your money, having clear financial goals can be the difference between just getting by and truly thriving. Whether you’re considering a debt relief application, saving for a new home, or planning for retirement, setting financial goals provides you with a roadmap for where you want to go. By creating a vision for your financial future and setting actionable steps to reach it, you can take control of your finances and build a life that’s financially secure.

But why exactly do financial goals matter? In a world filled with unexpected expenses and a fast-paced lifestyle, goals give you a sense of direction and purpose. They not only help you improve your financial situation, but also help you develop better spending and saving habits. In this article, we’ll explore why financial goals are essential and how they can help shape your financial future.

Financial Goals Help You Prioritize Your Spending

One of the main benefits of having financial goals is that they give you something to focus on. If you’re not sure where you want to be financially in the future, it can be easy to fall into the trap of impulsive spending. You might buy things you don’t need or put off saving because it feels like there’s always something more important to spend money on.

By setting clear financial goals, you can better prioritize how you spend your money. For instance, if you have a goal of reducing debt, you’ll know to focus on paying down high-interest credit cards rather than buying a new pair of shoes. Or, if saving for retirement is important to you, you can create a plan to consistently contribute to a retirement account instead of spending on things that don’t add value to your long-term happiness.

This prioritization doesn’t just apply to your personal finances. At work, having financial goals can help you be more mindful about how you manage your income, taxes, and other business-related expenses. Whether you’re running a small business or managing personal funds, being clear about your financial objectives can help you manage your cash flow more effectively.

Financial Goals Help You Reduce Debt

Debt can feel like a weight around your neck, preventing you from moving forward financially. It can take a toll on your mental and physical well-being, especially if you feel like you’re drowning in bills. But the good news is, by setting clear financial goals, you can start reducing your debt one step at a time.

If you’re facing a mountain of credit card bills or loans, a debt relief application might be an option to help get your finances back on track. Debt relief options, like consolidating loans or negotiating with creditors, can help you reduce interest rates and pay off your debt faster. Having clear financial goals will guide you on how much to pay off each month, and help you focus your energy on clearing up the most urgent debts first.

By setting realistic and achievable debt reduction goals, you can eliminate high-interest debt and start saving for the future instead of being buried under monthly payments. Once your debt is under control, you’ll have more financial freedom, and you can focus on building your savings and preparing for long-term goals like homeownership or retirement.

They Make Saving for the Future Easier

Saving money can feel like an impossible task, especially when living paycheck to paycheck. But having financial goals in place can make saving feel much more achievable. When you have specific objectives, such as saving for a new car, a down payment on a house, or your retirement, it gives you a reason to save. Instead of putting money aside without any clear purpose, you’ll be saving with intention.

For example, if you’re planning to buy a home in the next few years, setting a goal to save a specific amount each month for a down payment can help you stay on track. Likewise, if you’re concerned about your future and retirement, establishing a goal to contribute to a 401(k) or IRA can set you on the right path to a comfortable retirement.

By breaking down larger financial goals into smaller, more manageable steps, you’ll be able to see your progress and stay motivated to keep saving. The key is consistency—once you establish the habit of saving regularly, it becomes easier to build your financial security over time.

Setting Goals Helps You Prepare for Life’s Unexpected Costs

Life is full of surprises. Whether it’s an unexpected medical bill, a car repair, or a job loss, having a financial cushion can make all the difference when an emergency arises. Without a clear savings goal, these unexpected costs can leave you scrambling to find money, which often results in debt.

With proper planning, you can set financial goals that include building an emergency fund. Financial experts typically recommend having three to six months’ worth of expenses saved in case of a job loss or emergency. While this can seem like a daunting task, setting small savings goals can make it more manageable. For example, you might start by saving $100 a month and gradually increase your savings as you adjust your budget and spending habits.

Once you’ve built your emergency fund, you’ll feel more secure knowing you can handle unexpected expenses without resorting to credit cards or loans. In addition, an emergency fund can prevent you from using debt to cover these expenses, saving you money on interest payments and helping you maintain good credit.

The Emotional Benefits of Financial Goals

It’s easy to overlook the emotional benefits of having financial goals. Managing money can often be stressful, especially when there’s no clear plan in place. Financial goals give you peace of mind and help reduce anxiety about your financial future. Knowing that you’re working towards specific goals, whether it’s getting out of debt or saving for a big purchase, provides a sense of accomplishment and control.

With clear financial goals, you’re less likely to be caught off guard by unexpected expenses or feel lost when making decisions about your money. Having financial goals also helps you stay disciplined with your spending, as you’ll be focused on your long-term objectives instead of giving in to impulse buys.

Conclusion

Financial goals matter because they provide direction and structure for your financial life. Whether you’re working on reducing debt, saving for a home, or planning for retirement, having clear goals helps you stay on track and make better decisions with your money. They allow you to focus on what’s important and help you prioritize your spending and saving.

If you’ve struggled with managing your money in the past, now is the perfect time to start setting financial goals. These goals not only help improve your financial situation but also give you the confidence to handle life’s challenges with financial stability. By creating a plan, sticking to your goals, and adjusting as needed, you can achieve your dreams and secure a bright financial future.