If you’ve ever felt overwhelmed by your finances, figuring out how to budget might seem like a daunting task. With all the different expenses, savings goals, and financial priorities to balance, it’s hard to know where to start. That’s where the 50/30/20 budget comes in. It’s a simple and effective way to divide up your money, so you’re not only paying your bills but also saving for the future and allowing room for some fun.

The beauty of this budgeting rule is that it’s not rigid—it’s flexible and can be adapted to fit various financial situations. Whether you’re trying to reduce debt, save for something big, or just get your spending in check, the 50/30/20 rule gives you a structure to make sure your money is working for you. In this article, we’ll break down the 50/30/20 rule, explain how it can work for you, and show you how to apply it to your own finances.

What is the 50/30/20 Budget?

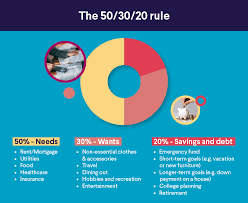

The 50/30/20 budget rule is a straightforward guideline that divides your after-tax income into three main categories: needs, wants, and savings. The idea is to give you a balanced approach to managing your money.

- 50% for Needs

This category includes all the things you absolutely need to live, such as housing, utilities, groceries, and transportation costs. These are expenses that you can’t easily avoid or reduce. If you’re working through debt resolution programs, this category might also include debt repayments, like credit card bills or personal loans. - 30% for Wants

These are non-essential things that you’d like to have but can live without. Think of things like dining out, entertainment, subscriptions, shopping, and vacations. While these are nice to have, they are not essential to your day-to-day living. The 30% for wants gives you the flexibility to enjoy life and have fun without overspending. - 20% for Savings and Debt Repayment

The final part of the rule directs 20% of your income toward savings or paying off debt. This could include contributions to an emergency fund, retirement savings (like a 401(k) or IRA), or putting money toward long-term goals. If you have high-interest debt, such as credit cards or personal loans, this portion of your budget can also go toward making extra payments to reduce that debt faster.

The beauty of this method lies in its simplicity. Instead of trying to track every little purchase, it helps you focus on three major categories: essentials, lifestyle, and future planning. It also helps keep you balanced by ensuring you’re not over-prioritizing spending on things you want, at the expense of saving or paying down debt.

How to Apply the 50/30/20 Budget to Your Finances

The first step in applying the 50/30/20 budget is to figure out how much you’re earning after taxes. This is the money you have to work with. Once you know your after-tax income, you can start to allocate it based on the 50/30/20 formula.

- Calculate Your Needs

To find 50% of your after-tax income, start by adding up all your necessary expenses. This includes rent or mortgage, utilities, groceries, car payments, insurance, transportation, and minimum debt payments. These are non-negotiable expenses that you need to survive. If your needs exceed 50% of your income, you may need to reassess your spending in this area to find savings opportunities. - Allocate 30% for Wants

Next, calculate 30% of your after-tax income. This is the money that can go toward anything you want—going out with friends, entertainment, travel, or a shopping spree. While this is not as essential as your needs, it’s important to have this category so you can enjoy life and treat yourself. Keep in mind that living within this 30% might require making some sacrifices in non-essential areas, such as cutting back on subscription services or eating out less often. - Focus 20% on Savings or Debt Repayment

Lastly, set aside 20% of your income for savings or paying off debt. If you don’t have high-interest debt, this portion can go directly into a savings account, retirement fund, or other investment vehicles. If you’re currently in a debt resolution program, prioritize using this 20% to reduce your debt burden. Once your debt is under control, you can redirect these funds into long-term savings.

The key here is to be realistic. If you find that 50% of your income is not enough to cover your needs, you might need to make adjustments in your lifestyle. Alternatively, if you have high debt, you may want to focus more on paying off debts before allocating as much to savings.

Benefits of the 50/30/20 Budget

The 50/30/20 rule offers several benefits that can help you achieve financial stability and peace of mind:

- Clarity and Simplicity

The 50/30/20 budget is incredibly simple to follow. There’s no need to track every small purchase, and it doesn’t require advanced financial knowledge. Just divide your income into three broad categories, and you’ll have a clear picture of where your money is going. - Flexibility

Life changes, and so do your financial priorities. The beauty of this budgeting method is that it can be easily adjusted. If you’re focusing on paying off debt, for example, you can temporarily increase the percentage allocated to debt repayment and decrease the amount for wants. If you have extra income, you can put more toward savings. - Balanced Approach to Financial Health

By splitting your income into needs, wants, and savings, you ensure that you’re balancing your present enjoyment with future financial security. It also helps prevent overspending, as you won’t spend more than what’s allocated to each category. - Avoiding Debt Accumulation

One of the key reasons people struggle financially is because they let lifestyle expenses (wants) consume too much of their budget. The 50/30/20 rule prevents that by capping your non-essential spending to 30%, leaving you with more room to pay down debt or build savings.

Challenges of the 50/30/20 Budget

While the 50/30/20 budget is an excellent framework for many people, there are some challenges you may face:

- Adjusting to Fixed Expenses

In some cases, your fixed expenses (needs) may be higher than expected, especially in places with a high cost of living. If your needs exceed 50%, you may need to reevaluate your wants category or try to reduce your expenses, such as moving to a less expensive home or cutting back on transportation costs. - High Debt Levels

If you have significant debt, 20% may not be enough to pay it off quickly. In this case, focusing more on paying off your debt first and adjusting the 50/30/20 split can help you get back on track faster. - Balancing Lifestyle and Savings

It can be tough to stick to the 30% allocated for wants, especially when you’re trying to maintain a social life or enjoy some luxuries. The key is to stay mindful of your financial goals and ensure that your short-term desires don’t outweigh your long-term stability.

Conclusion: Why the 50/30/20 Budget Works

The 50/30/20 budget is a flexible and effective way to manage your finances. By allocating your money across three categories—needs, wants, and savings or debt repayment—you can create a balanced financial plan that works for your lifestyle and goals. Whether you’re working on paying off debt or saving for a future purchase, this simple strategy can help you take control of your finances, avoid unnecessary spending, and achieve long-term financial health.