Buying your first home is an exciting milestone—a blend of anticipation, pride, and maybe a bit of nervousness. As thrilling as it is, the process can feel overwhelming, with financial decisions, legal paperwork, and home maintenance responsibilities all competing for your attention. To make the journey smoother, it’s crucial to approach homeownership with a plan.

Whether you’re just beginning your search or have already signed on the dotted line, these five essential tips will help you navigate the process with confidence.

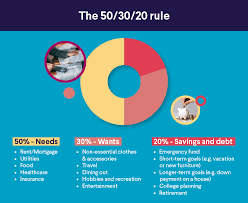

1. Set a Realistic Budget

Before you begin house hunting, determine how much home you can afford. A clear budget prevents you from falling in love with properties that are outside your price range and ensures you don’t overextend yourself financially.

Start by calculating your monthly income and expenses. Experts recommend that your mortgage payment—including principal, interest, taxes, and insurance—should not exceed 28% of your gross monthly income.

Don’t forget to account for other costs associated with homeownership, such as:

- Closing Costs: Typically 2–5% of the home’s purchase price.

- Maintenance: Repairs, landscaping, and upkeep.

- Utilities: Water, electricity, gas, and internet.

Setting a budget early helps you approach your purchase with financial clarity and peace of mind.

2. Prioritize Location Over Features

While it’s tempting to focus on home features like granite countertops or walk-in closets, the location of your home is equally, if not more, important. You can always renovate or upgrade your home’s interior, but you can’t change its location.

When choosing a neighborhood, consider:

- Proximity to work, schools, and public transportation.

- Access to essential amenities like grocery stores, hospitals, and parks.

- Safety and overall community vibe.

Visit the area at different times of the day to assess traffic, noise levels, and overall livability. Investing in a home in a desirable location can also yield better long-term returns if you decide to sell.

3. Understand the Importance of Home Inspections

A home may look perfect on the surface, but unseen issues could turn your dream purchase into a costly nightmare. Before finalizing your purchase, hire a licensed home inspector to thoroughly examine the property.

A professional inspection typically includes an evaluation of:

- Structural integrity (foundation, walls, and roof).

- Electrical and plumbing systems.

- HVAC (heating, ventilation, and air conditioning) systems.

- Potential pest or mold issues.

While inspections involve an upfront cost, they can save you from significant repair expenses in the future. If the inspection reveals issues, you may be able to negotiate repairs or a lower purchase price with the seller.

4. Secure Home Insurance

One of the most critical steps for first-time homeowners is obtaining a comprehensive home insurance policy. While it’s often required by mortgage lenders, home insurance is more than just a box to check—it’s a safeguard for your investment.

Why Home Insurance Is Essential

- Protects Your Home and Belongings: A good policy covers damage to your home caused by events like fires, storms, or theft. This protection extends to personal belongings, such as furniture and electronics.

- Liability Coverage: If someone is injured on your property, your home insurance can cover medical bills or legal fees, sparing you from significant out-of-pocket expenses.

- Covers Additional Living Expenses: If your home becomes uninhabitable due to a covered event, your policy can pay for temporary housing and other related costs.

How to Choose the Right Policy

Compare policies from multiple providers to find one that fits your needs and budget. Look for features like customizable coverage, discounts for home security systems, and clear terms about what’s covered and excluded.

Investing in home insurance not only protects your property but also gives you peace of mind as you settle into your new home.

5. Build an Emergency Fund for Maintenance and Repairs

Owning a home comes with the responsibility of keeping it in good condition. Unlike renting, where landlords handle repairs, homeowners are responsible for fixing issues as they arise.

Building an emergency fund specifically for home maintenance ensures you’re financially prepared for unexpected expenses, such as:

- Replacing a leaking roof.

- Fixing a broken HVAC system.

- Addressing plumbing or electrical problems.

Experts recommend setting aside 1–3% of your home’s value annually for maintenance. For instance, if your home costs $250,000, aim to save $2,500 to $7,500 per year. Regular upkeep not only prevents costly emergencies but also helps preserve your home’s value over time.

Bonus Tips for First-Time Homeowners

- Stay Organized: Keep all home-related documents, such as warranties, manuals, and repair receipts, in one place for easy reference.

- Learn Basic DIY Skills: Knowing how to handle minor repairs, like fixing a leaky faucet or patching drywall, can save you time and money.

- Explore Tax Benefits: As a homeowner, you may qualify for tax deductions on mortgage interest and property taxes. Consult a tax professional to maximize your benefits.

Conclusion

Buying your first home is a significant milestone that comes with both excitement and responsibility. By setting a budget, choosing the right location, prioritizing inspections, securing home insurance, and preparing for maintenance, you can ensure a smooth transition into homeownership.

Home insurance plays a vital role in protecting your investment and giving you peace of mind. While it may seem like an added expense, the financial security it offers in the face of unexpected events makes it an invaluable step for every first-time homeowner.

With thoughtful planning and these tips in mind, you’ll be well on your way to turning your first house into a home you love and cherish.